Modeling stock returns’ volatility with ARCH models

In this recipe, we approach the problem of modeling the conditional volatility of stock returns with the Autoregressive Conditional Heteroskedasticity (ARCH) model.

To put it simply, the ARCH model expresses the variance of the error term as a function of past errors. To be a bit more precise, it assumes that the variance of the errors follows an autoregressive model. The entire logic of the ARCH method can be represented by the following equations:

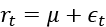

The first equation represents the return series as a combination of the expected return μ and the unexpected return  .

.  has white noise properties—the conditional mean equal to zero and the time-varying conditional variance

has white noise properties—the conditional mean equal to zero and the time-varying conditional variance  .

.

Error terms are serially uncorrelated but do not need to be serially independent, as they can exhibit conditional heteroskedasticity.

is also known as the mean-corrected return, error term, innovations...

is also known as the mean-corrected return, error term, innovations...