The following list shows our agenda and the next stage is the preparation of the cash flow statement:

- Record the historical profit and loss and balance sheet

- Calculate the historical growth drivers

- Project the growth drivers for the profit and loss accounts and balance sheet

- Build up the projected profit and loss accounts and balance sheet

- Prepare the asset and depreciation schedule

- Prepare the debt schedule

- Prepare the cash flow statement

- Ratio analysis

- DCF valuation

- Other valuations

- Scenario analysis

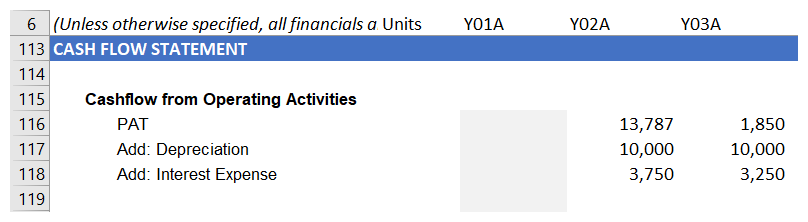

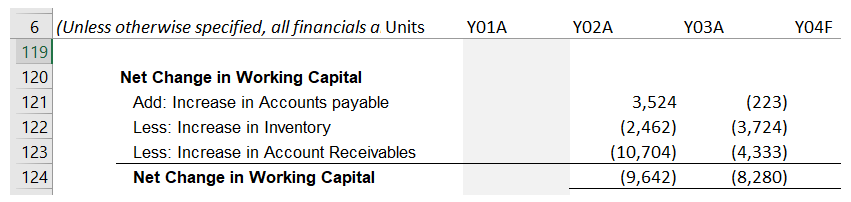

At this stage, we have completed the profit and loss account and the only item left to complete the balance sheet, which is still out of balance, is cash. In this chapter, we will look at how to prepare the cash flow statement for our project.

In this chapter, we will cover the following topics:

- Introduction to the cash flow statement

- Items not involving...