Chapter 8. Extreme Value Theory

The risk of extreme losses is at the heart of many risk management problems both in insurance and finance. An extreme market move might represent a significant downside risk to the security portfolio of an investor. Reserves against future credit losses need to be sized to cover extreme loss scenarios in a loan portfolio. The required level of capital for a bank should be high enough to absorb extreme operational losses. Insurance companies need to be prepared for losses arising from natural or man-made catastrophes, even of a magnitude not experienced before.

Extreme Value Theory (EVT) is concerned with the statistical analysis of extreme events. The methodology provides distributions that are consistent with extreme observations and, at the same time, have parametric forms that are supported by theory. EVT's theoretical considerations compensate the unreliability of traditional estimates (caused by sparse data on extremes). EVT allows the quantification of...

Let the random variable X represent the random loss that we would like to model, with F(x) = P(X ≤ x) as its distribution function. For a given threshold u, the excess loss over the threshold Y = X – u has the following distribution function:

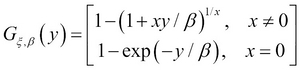

For a large class of underlying loss distributions, the Fu(y) distribution of excess losses over a high threshold u converges to a Generalized Pareto distribution (GPD) as the threshold rises toward the right endpoint of the loss distribution. This follows from an important limit theorem in EVT. For details, the reader is referred to McNeil, Frey, and Embrechts (2005). The cumulative distribution function of GPD is the following:

Here ξ is generally referred to as the shape parameter and β as the scale parameter.

Though strictly speaking, the GPD is only the limiting distribution for excess losses over a high threshold, however, it serves as the natural model of the excess loss distribution even for finite thresholds. In other words...

Application – modeling insurance claims

In the remainder of this chapter, we work through an example of using EVT in a real-life risk management application. We apply the preceding methodology to fire insurance claims, with the aims of fitting a distribution to the tails and providing quantile estimates and conditional expectations to characterize the probability and magnitude of large fire losses. We note that the exact same steps may be applied to credit losses or operational losses as well. For market risk management problems, where the underlying data is generally the return of a security, we would remove the gains from the data set and focus on the losses only; otherwise, the modeling steps are again identical.

Multiple packages are available in R for extreme value analysis. In this chapter we present the evir package in the following command. A good overview of the various R packages for EVT is provided in Gilleland, Ribatet, and Stephenson (2013).

As done previously, we need to install...

In this chapter, we presented a case study of how Extreme Value Theory methods can be used in R in a real-life risk management application. After briefly covering the theory of threshold exceedance models in EVT, we worked through a detailed example of fitting a model to the tails of the distribution of fire insurance claims. We used the fitted model to calculate high quantiles (Value at Risk) and conditional expectations (Expected Shortfall) for the fire losses. The presented methods are readily extendable to market, credit, or operational risk losses as well.